Navigating the complexities of preparing financial statements for an audit can feel daunting, but understanding the process is crucial for maintaining financial integrity and ensuring a smooth audit experience. This guide provides a comprehensive overview of the key steps involved, from preparing the balance sheet and income statement to addressing audit adjustments and leveraging financial statement analysis for proactive preparation.

We’ll demystify the process, offering practical advice and insights to help you confidently approach your next audit.

The preparation of accurate and reliable financial statements is not merely a compliance exercise; it’s a cornerstone of sound financial management. This guide will equip you with the knowledge and tools to produce financial statements that clearly reflect your organization’s financial position, performance, and cash flows, thus fostering trust with stakeholders and providing a solid foundation for informed decision-making.

Preparing the Balance Sheet

The balance sheet, a cornerstone of financial reporting, provides a snapshot of a company’s financial position at a specific point in time. It’s crucial for understanding a company’s assets, liabilities, and equity, and is therefore a key focus during an audit. A well-prepared balance sheet, accurately reflecting the financial reality of the business, is essential for generating reliable financial statements.

This section details the key components and verification methods involved in preparing a balance sheet for audit purposes.

Balance Sheet Components and Their Audit Importance

The balance sheet adheres to the fundamental accounting equation: Assets = Liabilities + Equity. Each component plays a vital role and requires thorough scrutiny during an audit. Assets represent what a company owns (e.g., cash, accounts receivable, inventory, property, plant, and equipment). Liabilities represent what a company owes to others (e.g., accounts payable, loans payable). Equity represents the owners’ stake in the company (e.g., retained earnings, contributed capital).

The auditor’s verification of these components ensures the balance sheet accurately reflects the company’s financial health and compliance with accounting standards. Inaccurate or misrepresented information in any of these areas can significantly impact the overall reliability of the financial statements.

Methods for Verifying Asset Valuations

Verifying asset valuations is a critical aspect of the audit process. Different methods are used depending on the nature of the asset. For example, cash balances can be verified through bank reconciliations, comparing the company’s records with bank statements. Accounts receivable can be verified through confirmations sent directly to customers, requesting verification of outstanding balances. Inventory valuation often involves physical counts and observation of inventory management procedures, with the auditor potentially using statistical sampling techniques for large inventories.

Property, plant, and equipment (PP&E) valuations often require reviewing depreciation schedules, appraisals, and purchase documentation. The auditor uses various techniques to ensure the valuation of each asset is appropriate and in line with generally accepted accounting principles (GAAP). For instance, the auditor may use the lower of cost or market method to verify inventory valuation, ensuring the inventory is not overstated.

Sample Balance Sheet

The following is a sample balance sheet presented in a format suitable for audit purposes. Note that this is a simplified example and a real-world balance sheet would be far more detailed.

| Balance Sheet as of December 31, 2023 | |

|---|---|

| Assets | |

| Current Assets: | |

| Cash | $10,000 |

| Accounts Receivable | $20,000 |

| Inventory | $30,000 |

| Total Current Assets | $60,000 |

| Non-Current Assets: | |

| Property, Plant, and Equipment (Net) | $40,000 |

| Total Assets | $100,000 |

| Liabilities and Equity | |

| Current Liabilities: | |

| Accounts Payable | $15,000 |

| Total Current Liabilities | $15,000 |

| Non-Current Liabilities: | |

| Long-term Debt | $25,000 |

| Total Liabilities | $40,000 |

| Equity: | |

| Retained Earnings | $60,000 |

| Total Equity | $60,000 |

| Total Liabilities and Equity | $100,000 |

Preparing the Income Statement

The income statement, also known as the profit and loss statement, presents a company’s financial performance over a specific period. Preparing an income statement for audit requires meticulous attention to detail and adherence to generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS), depending on the jurisdiction. A well-prepared income statement provides a clear and accurate picture of a company’s revenue, expenses, and ultimately, its profitability.Preparing an income statement that meets audit standards involves systematically classifying and summarizing all revenues and expenses.

This includes ensuring proper revenue recognition, accurate cost allocation, and appropriate treatment of non-operating items. Auditors scrutinize the income statement for potential misstatements or manipulations, focusing on areas where subjective judgments or estimations are involved. The process requires careful documentation and a robust internal control system to support the reported figures.

Revenue Recognition

Accurate revenue recognition is crucial for a reliable income statement. Misstatements in this area can significantly impact the company’s reported profitability and potentially mislead investors and stakeholders. Best practices for ensuring the accuracy and reliability of revenue recognition include:

- Applying the five-step model (or equivalent under IFRS) to ensure revenue is recognized when control of goods or services is transferred to the customer.

- Maintaining detailed records of sales transactions, including contracts, invoices, and payment receipts.

- Implementing robust internal controls to prevent revenue manipulation, such as segregation of duties and regular reconciliation of sales data.

- Establishing clear revenue recognition policies and procedures that are consistently applied across all business segments.

- Performing regular reviews of revenue recognition practices to identify and address potential weaknesses or inconsistencies.

Potential Areas of Misstatement or Manipulation

Several areas within the income statement are susceptible to misstatement or manipulation. These often involve estimations or judgments, offering opportunities for intentional or unintentional errors. Examples include:

- Revenue Recognition Timing: Accelerating revenue recognition before the transfer of control or delaying it beyond the appropriate period can artificially inflate or deflate profits.

- Expense Recognition: Capitalizing expenses that should be expensed or vice-versa can significantly impact profitability. For example, inappropriately capitalizing research and development costs can inflate net income in the current period.

- Inventory Valuation: Using inappropriate inventory valuation methods (e.g., FIFO, LIFO, weighted-average cost) can distort the cost of goods sold and, consequently, gross profit.

- Depreciation and Amortization: Choosing an inappropriate depreciation or amortization method or using unrealistic useful lives can affect the reported expenses and profitability.

- Bad Debt Expense: Underestimating or overestimating the allowance for doubtful accounts can impact net income.

Internal Controls and Documentation

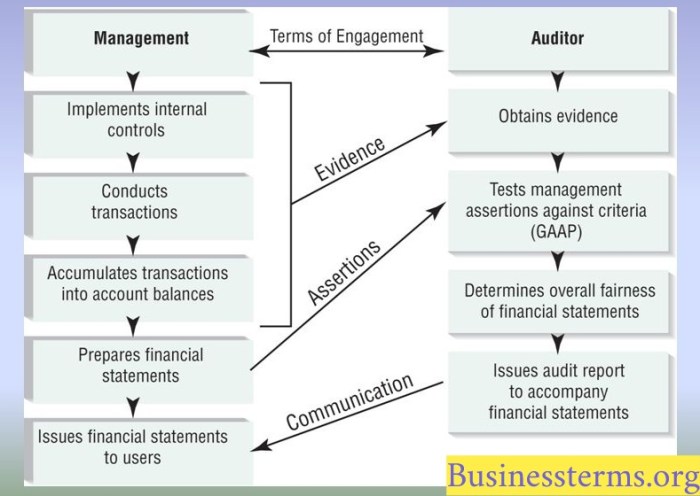

Robust internal controls are fundamental to the preparation of reliable financial statements. They provide assurance that financial data is accurate, complete, and free from material misstatement, thereby enhancing the credibility of the financial reporting process and reducing the risk of fraud. Strong internal controls also streamline the audit process, making it more efficient and less time-consuming.The documentation supporting financial statements during an audit serves as evidence of the accuracy and reliability of the reported figures.

It provides auditors with the necessary information to verify the assertions made in the financial statements and to assess the effectiveness of the company’s internal control system. Adequate documentation minimizes disputes and increases the overall confidence in the financial reporting process.

Essential Internal Controls Related to Financial Reporting

A well-designed system of internal controls minimizes the risk of errors and irregularities in financial reporting. The following checklist Artikels key internal controls that should be in place:

- Authorization of Transactions: All transactions should be properly authorized by individuals with appropriate levels of authority. This prevents unauthorized spending and ensures compliance with company policies.

- Segregation of Duties: Different individuals should be responsible for authorizing transactions, recording transactions, and custody of assets. This prevents fraud and minimizes the risk of errors.

- Independent Verification: Transactions should be independently verified to ensure accuracy and completeness. This can include reconciliations, reviews, and audits.

- Physical Safeguards over Assets: Physical assets should be properly secured to prevent theft or loss. This includes inventory controls, access restrictions, and regular physical counts.

- Documentation and Record Keeping: All financial transactions should be properly documented and maintained. This includes source documents, supporting schedules, and accounting records.

- Performance Reviews: Regular performance reviews should be conducted to assess the effectiveness of internal controls and identify areas for improvement. This helps maintain the integrity of the system.

- Information Technology Controls: Appropriate controls should be in place to safeguard the integrity of financial data stored electronically. This includes access controls, data backups, and disaster recovery plans.

Documentation Required for Audit Support

The documentation required to support the financial statements during an audit varies depending on the size and complexity of the organization. However, some essential documents include:

- General Ledger: The primary accounting record containing all financial transactions.

- Trial Balance: A summary of all general ledger accounts at a specific point in time.

- Supporting Schedules: Detailed schedules supporting specific line items in the financial statements.

- Source Documents: Original documents supporting transactions, such as invoices, receipts, and bank statements.

- Minutes of Meetings: Records of board and committee meetings.

- Contracts and Agreements: Agreements related to significant transactions.

- Internal Control Documentation: Documentation outlining the company’s internal control system.

Addressing Audit Adjustments and Findings

Responding effectively to audit adjustments and findings is crucial for ensuring the accuracy and reliability of financial statements. A well-managed response demonstrates a commitment to transparency and strengthens the relationship with the auditing firm. Proactive identification and correction of discrepancies minimizes potential disruptions and enhances the overall audit process.Understanding the nature of the audit adjustments and their potential implications is paramount.

The audit team will typically communicate their findings through a formal report, detailing discrepancies and suggesting necessary corrections. A timely and thorough response is essential to address these concerns effectively.

Common Audit Adjustments and Their Implications

Several common types of audit adjustments frequently arise during the audit process. These adjustments can stem from various sources, including errors in recording transactions, discrepancies in inventory valuation, or inconsistencies in revenue recognition. Understanding the implications of these adjustments is vital for rectifying the financial statements and preventing future occurrences.

| Adjustment Type | Description | Example | Implications |

|---|---|---|---|

| Inventory Valuation | Discrepancies between physical inventory count and recorded inventory levels. | A physical count reveals 100 units less than the recorded amount, resulting in an overstatement of inventory value. | Overstated assets on the balance sheet, potentially impacting the calculation of cost of goods sold and net income. |

| Revenue Recognition | Improper timing of revenue recognition, leading to misstatement of revenue in a particular period. | Revenue from a project completed in December was recorded in November, leading to an overstatement of November’s revenue and an understatement of December’s revenue. | Distorted picture of revenue trends, affecting financial ratios and potentially investor confidence. |

| Depreciation Expense | Incorrect application of depreciation methods or useful lives of assets. | Using a straight-line method when an accelerated method is more appropriate, leading to underestimation of depreciation expense. | Overstated net income and understated accumulated depreciation on the balance sheet. |

Correcting and Documenting Adjustments

The process of correcting and documenting adjustments requires a systematic approach to ensure accuracy and maintain a clear audit trail. This involves meticulously tracking each adjustment, its rationale, and the supporting documentation. This detailed record is essential for both internal control and for responding to auditor queries.

| Step | Action | Responsibility | Documentation |

|---|---|---|---|

| 1 | Review audit findings and supporting documentation. | Accounting team | Audit report, working papers |

| 2 | Prepare adjusting journal entries. | Accounting team | Journal entry, supporting calculations |

| 3 | Post adjusting entries to the general ledger. | Accounting team | Updated general ledger, trial balance |

| 4 | Prepare revised financial statements. | Accounting team | Revised financial statements, reconciliation |

| 5 | Communicate the corrections to the auditors. | Management | Letter of response to audit findings |

Preparing financial statements for audit requires meticulous attention to detail and a thorough understanding of accounting principles. By following the steps Artikeld in this guide, focusing on strong internal controls, and proactively analyzing your financial data, you can significantly reduce the risk of audit issues and enhance the overall efficiency of the audit process. Remember, well-prepared financial statements are not just a requirement for compliance; they are a testament to your organization’s financial health and a valuable asset in strategic planning.

FAQ Guide

What happens if discrepancies are found during the audit?

Discrepancies will typically lead to audit adjustments. The auditor will work with you to identify and correct these, documenting the process and any necessary changes to your financial statements.

How often should financial statements be prepared?

The frequency depends on your organization’s size and reporting requirements. Many companies prepare them annually, but some may do so quarterly or even monthly.

What is the role of an external auditor?

An external auditor provides an independent and objective assessment of your financial statements to ensure they are fairly presented and in accordance with applicable accounting standards.

What software can assist in preparing financial statements?

Numerous accounting software packages, ranging from simple spreadsheets to sophisticated enterprise resource planning (ERP) systems, can assist in preparing and managing financial statements.