Understanding financial audit findings and their effective reporting is crucial for maintaining financial health and transparency. This exploration delves into the process of identifying, documenting, and communicating audit findings to various stakeholders, from management to regulatory bodies. We will examine the impact of these findings on financial advice, planning, and the achievement of financial goals, highlighting best practices and ethical considerations along the way.

The implications of both material and immaterial findings will be analyzed, emphasizing the diverse types of findings encountered, including errors, irregularities, and even fraud. We’ll explore different reporting formats and visual representation techniques to ensure clarity and effective communication. The discussion will also cover the vital collaboration between financial auditors and advisors to ensure client benefit and compliance with regulations.

Reporting Financial Audit Findings

This section details the process of reporting financial audit findings, encompassing report design, stakeholder communication strategies, and a comparison of various reporting formats. Effective communication of audit findings is crucial for ensuring appropriate action is taken to address identified risks and improve financial controls.

Sample Financial Audit Report

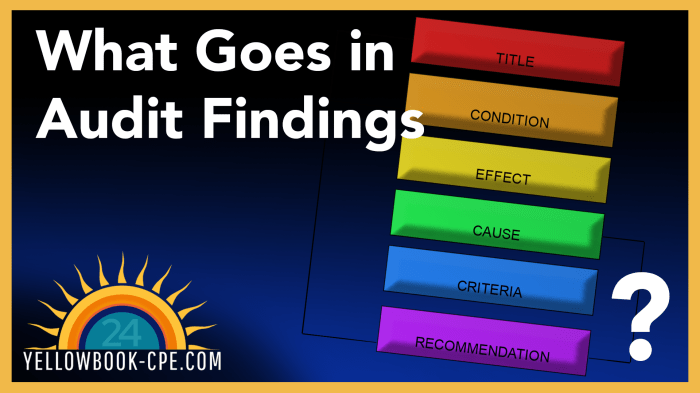

A comprehensive financial audit report typically includes the following sections:

Introduction

This section sets the context of the audit, identifying the entity audited, the period covered, the audit objectives, and the scope of the work performed. It should also state the applicable auditing standards followed. For example, an introduction might state: “This report presents the findings of the financial audit conducted on Acme Corporation for the fiscal year ended December 31, 2023.

The audit was performed in accordance with generally accepted auditing standards (GAAS).”

Methodology

This section Artikels the audit procedures followed, including the sampling methods used, the tests performed, and the overall audit approach. A description of the risk assessment process and any limitations encountered should also be included. For example: “The audit involved a combination of analytical procedures, tests of controls, and substantive testing of transactions and balances. A stratified random sampling technique was used for testing accounts receivable.”

Findings

This is the core of the report, detailing all significant findings identified during the audit. Each finding should be clearly stated, including the nature of the issue, the impact, and supporting evidence. Findings should be presented objectively and factually, avoiding subjective interpretations or opinions. For example: “A material weakness was identified in the internal control over cash disbursements, specifically the lack of segregation of duties in the processing of payments.

This weakness increases the risk of unauthorized payments.”

Recommendations

This section provides specific and actionable recommendations to address the findings identified. The recommendations should be realistic, achievable, and cost-effective. For example: “It is recommended that Acme Corporation implement a dual authorization process for all cash disbursements exceeding $5,000. Additionally, a review of existing segregation of duties policies and procedures is recommended.”

Best Practices for Communicating Financial Audit Findings

Effective communication is paramount. Tailoring the message to the audience is key. Management needs detailed information and action plans, while the audit committee requires a concise summary of key risks and management’s response. Regulatory bodies need compliance-focused reporting. Using clear, concise language, avoiding technical jargon, and providing visual aids where appropriate are all crucial for effective communication.

Comparison of Reporting Formats for Financial Audit Findings

The choice of reporting format depends on the audience and the complexity of the findings. A combination of formats is often most effective.

| Reporting Format | Advantages | Disadvantages | Suitable Audience |

|---|---|---|---|

| Narrative | Provides detailed explanation and context | Can be lengthy and difficult to digest | Management, Audit Committee (detailed reports) |

| Tabular | Presents data concisely and allows for easy comparison | May lack context and explanation | Audit Committee, Management (summary reports) |

| Graphical | Illustrates key findings visually, enhancing understanding | May oversimplify complex issues | Management, Audit Committee (summary reports) |

| Combination | Combines the strengths of different formats | Requires more effort in preparation | All stakeholders |

Impact of Financial Audit Findings on Financial Advice

Financial audit findings significantly influence the financial advice provided to clients. The nature and severity of these findings directly impact the reliability of the financial information used in the planning process, potentially necessitating adjustments to investment strategies, risk assessments, and overall financial goals. A thorough understanding of audit findings is crucial for financial advisors to provide accurate and responsible guidance.The weight given to audit findings depends on their materiality and the nature of the issues identified.

Material findings, those that could reasonably influence the decisions of users of the financial statements, necessitate a more significant response than immaterial ones. The type of finding also plays a role; for instance, a finding related to revenue recognition will have different implications than one concerning internal controls.

Materiality of Audit Findings and Financial Planning

Material audit findings, indicating significant misstatements or weaknesses in internal controls, directly impact financial planning strategies. For example, the discovery of significant unrecorded liabilities could necessitate a reassessment of a client’s net worth and adjustments to their retirement planning or investment portfolio allocation. Similarly, weaknesses in internal controls, especially those related to cash management, might lead to recommendations for improved financial record-keeping and budgeting practices.

Advisors may need to adjust investment strategies to account for increased risk profiles associated with the identified weaknesses. Conversely, immaterial findings, while still needing documentation, are less likely to trigger major shifts in financial planning. These might involve minor accounting errors that do not significantly affect the overall financial picture.

Types of Audit Findings and Their Implications

Different types of audit findings have varying implications for financial planning. Findings related to revenue recognition could impact projected income streams, affecting investment timelines or the feasibility of certain financial goals. Findings concerning asset valuation could lead to adjustments in portfolio diversification or risk tolerance levels. Findings related to liabilities, as mentioned previously, can impact net worth calculations and debt management strategies.

Audits revealing weaknesses in internal controls may necessitate recommendations for improved financial management practices, such as enhanced budgeting, cash flow forecasting, and risk mitigation strategies. The advisor’s role is to interpret the findings, assess their impact on the client’s financial situation, and adjust the financial plan accordingly.

Legal and Regulatory Ramifications of Mishandled Audit Findings

Failure to properly address or report significant audit findings carries significant legal and regulatory ramifications. Financial advisors have a fiduciary duty to act in the best interests of their clients, and ignoring material findings that could negatively impact their clients’ financial well-being constitutes a breach of this duty. This could lead to legal action, including lawsuits for negligence or malpractice.

Regulatory bodies, such as the Securities and Exchange Commission (SEC) or state-level regulatory agencies, could also impose penalties, including fines or suspension of licenses. For example, if an advisor fails to report a material misstatement in a client’s financial statements that leads to significant financial losses for the client, the advisor could face severe legal and regulatory consequences.

Transparency and responsible handling of audit findings are paramount for maintaining compliance and protecting both the advisor and the client.

Effective financial audit reporting is not merely a compliance exercise; it’s a cornerstone of sound financial management and proactive planning. By understanding the nuances of identifying, documenting, and communicating audit findings, organizations can mitigate risks, improve financial health, and achieve their long-term financial goals. The collaborative relationship between auditors and financial advisors is essential in this process, ensuring both accuracy and ethical considerations are prioritized for the benefit of all stakeholders.

FAQ Explained

What is the difference between a material and an immaterial audit finding?

A material finding is significant enough to influence the financial statements’ users’ decisions, while an immaterial finding is insignificant and unlikely to affect those decisions.

What should I do if I discover a potential fraud during an audit?

Immediately report your findings to the appropriate authorities within the organization and potentially external regulatory bodies, depending on the severity and nature of the suspected fraud.

How can I ensure my audit report is easily understood by non-financial stakeholders?

Use clear, concise language, avoid technical jargon, and utilize visual aids such as charts and graphs to present complex information in a digestible format.

What are the potential legal consequences of ignoring audit findings?

Ignoring significant audit findings can lead to legal repercussions, including fines, penalties, and even criminal charges, depending on the jurisdiction and the nature of the findings.